by Paul Hoffmeister, Portfolio Manager and Chief Economist

Viewed through the lens of the Strait of Hormuz, the recent conflict with Iran is not simply a regional conflict, but a global macroeconomic shock transmitted through a single, critical chokepoint.

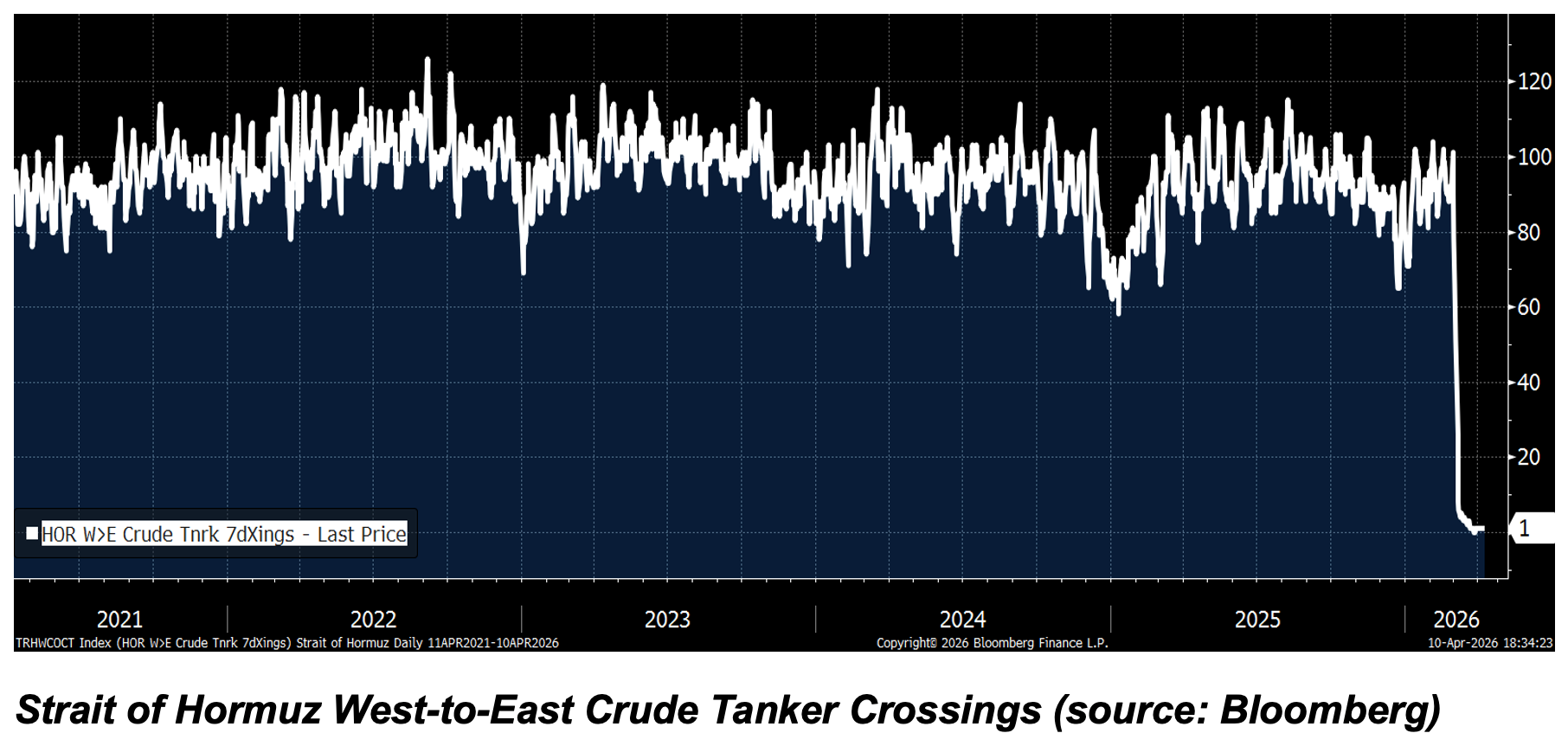

According to the Joint Maritime Information Centre, an average of 138 ships usually pass through the Strait every day. But Bloomberg data indicates that since the onset of the military conflict on February 28th, the number of tankers has fallen to less than 10 per day, and even zero on some days.

The Strait concentrates an outsized share of the world’s oil and LNG flows among many other vital resources including chemical products, fertilizers, helium and aluminum. As a result of this recent supply shock, a rapid and broad-based repricing has occurred across energy markets, inflation expectations, growth forecasts, and financial assets.

One of the most obvious and immediate effects has been on the price of oil. Its forward price curve has shifted upward, reflecting not only supply tightness but a sustained geopolitical risk premium tied to the disruption in the Strait. This has already translated into higher gasoline prices, reinforcing a direct transmission channel from geopolitics to the consumer. According to AAA, the national average price for a gallon of regular unleaded gasoline has jumped from approximately $2.98 in late February to more than $4.10 today. In economic terms, this price increase functions as a tax: it raises input costs across industries while eroding real household purchasing power.

From this vantage point, the broader implications for inflation and growth can be seen. Inflation expectations have moved meaningfully higher. The 5-year breakeven inflation rate, a market-based measure of expected average inflation over the next 5 years, has increased from approximately 2.45% in late February to nearly 2.65% today. The Cleveland Fed Inflation Nowcast suggests that CPI inflation will increase approximately 3.6% during the next year, whereas in February, it was expecting a 2.4% increase. Importantly, this is not simply a reaction to current price levels; it represents a repricing of the forward inflation path, driven by the recognition that natural resource supply risk is now structurally elevated.

At the same time, growth expectations have deteriorated. The Atlanta Fed GDPNow Forecast shows that real GDP growth decelerated from nearly 3.0% in late February to 1.3% currently. The St. Louis Fed Economic News Index suggests that real GDP is currently growing at 2%, from almost 3% in February.

The measurable drag on economic activity indicated by high-frequency GDP trackers such as these likely reflects both direct effects, such as higher costs and reduced real income, and second-order effects, including weaker business and consumer confidence. Yet the data stops short of signaling an outright recession. Instead, it points to an economy that is slowing but still expanding.

This combination of rising inflation alongside weakening growth defines the current environment. It is not a demand-driven overheating cycle, but a supply-driven stagflationary impulse, originating from the risks embedded in the Strait of Hormuz. That dynamic is now shaping monetary policy expectations. Markets have adjusted their views on the path of the Federal Reserve, as reflected in shifts in implied year-end policy rates. In February, markets were expecting two quarter point rate cuts as the most likely scenario by year-end; now, markets appear to believe that no rate cuts are the most likely outcome.

The Fed faces a complex tradeoff in their policy formulation: tighten policy to contain inflation risks and amplify the growth slowdown; or ease and risk entrenching higher inflation.

Fixed income markets reflect some of this tension. Treasury yields, particularly at the long end, have been volatile as investors reassess both inflation risks and the appropriate term premium in a more uncertain environment. The 10-year Treasury yield has notably jumped from less than 4% in late February to more than 4.33% today.

Equity markets, meanwhile, have exhibited significant dispersion rather than uniform decline. According to Bloomberg, industry-level performance between late February and early April shows a pattern consistent with this new inflation and growth regime: many energy-linked and defensive industries outperformed, while more cyclical and rate-sensitive areas lagged. This suggests that investors were not pricing an imminent recession, but rather a shift toward slower growth, higher inflation, and greater volatility.

An important overlay to all of this is the role of expectations. Prediction markets and other forward-looking indicators show a sharp rise in perceived recession risk, even as hard data has yet to confirm it. This may highlight a feature of modern markets: expectations adjust faster than fundamentals, and those expectations themselves can influence financial conditions and economic behavior.

In sum, the resource supply shock out of the Strait of Hormuz can be an organizing framework for understanding the current macroeconomic environment. A localized geopolitical risk has cascaded through energy markets into inflation, through inflation into policy uncertainty, and through policy into financial conditions and asset prices. The economy now sits in a more fragile equilibrium: growth is slowing but intact, inflation is rising, and the range of potential outcomes has widened. What has changed most is not just the level of key variables, but the distribution of risks, all of which now trace back, directly or indirectly, to the vulnerability embedded in that narrow passage of water.

Paul Hoffmeister is Chief Economist and Portfolio Manager at Camelot Portfolios, managing partner of Camelot Event-Driven Advisors (CEDA), and co-portfolio manager of the Camelot Event-Driven Fund (EVDIX • EVDAX).

WANT MORE WAYS TO STAY UP-TO-DATE

ON ALL THE EVENT-DRIVEN NEWS?

FOLLOW US ON LINKEDIN!

VISIT OUR FRIENDS AT EVENT-DRIVEN.BLOG

Camelot Event-Driven Advisors LLC | 1700 Woodlands Drive | Maumee, OH 43537

All investing carries with it risk, including the risk of loss, that investors should be prepared to bear. This material is for educational use only and is not intended to be construed as investment advice. Readers or participants in an oral presentation of these materials should consult with their own personal financial, tax, legal and other advisors before making any decision to make any investment, including any investment believed to be related to the topics of these materials. The discussion herein, while based on current economic data, may or may not lead to the outcomes presented, express or implied. Economic conditions, even in a single sector, are subject to an unknown number of variables, the totality of which are impossible to predict or account for in analytical assumptions. Past performance does not necessarily lead to future results. Specifically, trends in economic data do not always, and frequently do not, continue as expected. B727

Copyright © 2026 Camelot Event-Driven Advisors LLC, All rights reserved.

Copyright © 2026 Camelot Portfolios LLC, All rights reserved.