by Paul Hoffmeister, Chief Economist

Some Covid case numbers stopped improving.

The Federal Reserve began to telegraph a shift away from its current easy money policy.

A concerted effort is underway to raise corporate tax rates around the world.

Following Vice President Kamala Harris’s trip to Central America, her political prospects in 2024 took a notable turn for the worse in betting markets. However, President Biden’s probability of being the 2024 Democratic nominee improved.

From our perspective, it’s a relatively quiet and positive market environment these days. The CBOE Volatility Index reached a Covid low; the S&P 500 is up over 15% year-to-date; credit spreads such as the Moody’s Baa-Aaa spread is tighter than it was in at the beginning of 2020; and the number of Americans filing for unemployment benefits has reached its lowest levels since the start of the pandemic.

Despite the steady, favorable trends and it being the middle of summer, a number of significant events occurred during the last month that may have larger implications in the coming months. Some Covid case numbers stopped improving. The Federal Reserve began to telegraph a shift away from its current easy money policy. A concerted effort is underway to raise corporate tax rates around the world. And, Vice President Kamala Harris’s political prospects took a turn for the worse following her trip to Central America.

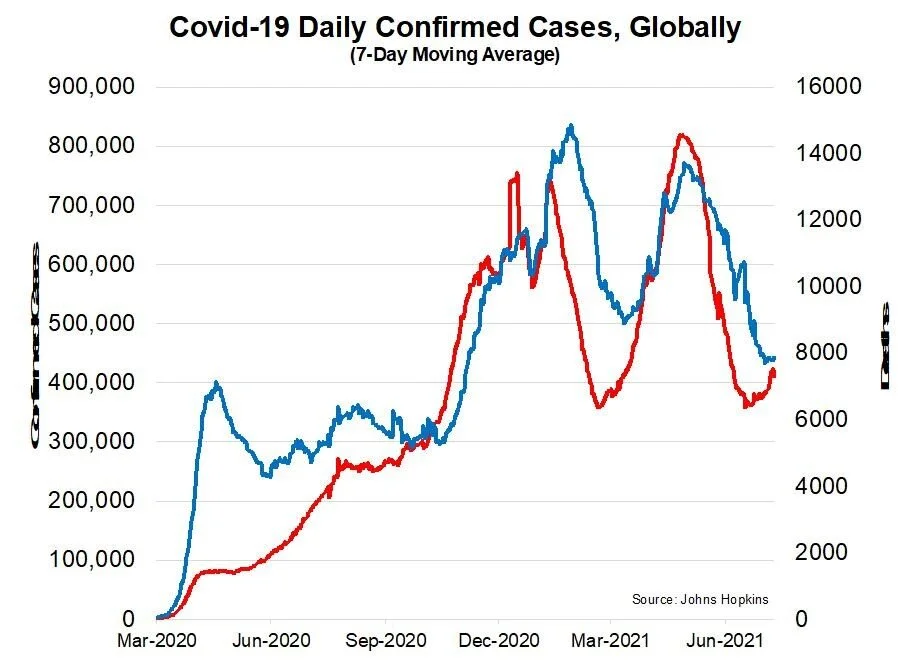

Covid

Since mid-June, the 7-day moving average of new Covid cases each day around the world has increased from approximately 360,000 to 420,000 – according to Johns Hopkins. This comes after the steep decline in daily case counts from over 800,000 since late April. Based on the Johns Hopkins data, the increases are primarily coming from the UK, South Africa, Russia, India, and Indonesia.

Similar to what happened in March after confirmed cases increased, many expect the death toll to increase in the coming month. For the most part, lockdown restrictions around the world have eased; but if the current trend in the Covid numbers continues, it certainly raises the risk of extended or reimposed lockdowns.

Fed Policy

On June 16, following its two-day policy meeting, the FOMC raised its inflation forecast from 2.4% to 3.4%, and a number of members conveyed that they expect at least two quarter-point rate increases by the end of 2023. In March, no officials expected a lift off from today’s zero interest rate policy until 2024.

While the news sparked a slight weakness in equities during the afternoon of the announcement (the S&P fell about 70 basis points at one point), the most pronounced moves occurred in the Treasury and gold markets.

The last time that the Fed attempted to normalize policy was 2018, and the market panic at the time strongly argued that the Fed failed in both implementing the correct policy course and effectively telegraphing central bank policy. This and the unique pandemic circumstance today don’t leave a lot of room for error for the FOMC today.

For now, the FOMC is telegraphing a change in policy more than 2 years from now. And Chairman Powell stated in the post-meeting press conference, “This is an extraordinarily unusual time, and we really don't have a template or any experience in a situation like this.”

It appears that the Fed communication strategy is to give itself significant lead time to communicate a policy change while being transparent that it simply doesn’t know its policy path, at least with a high degree of conviction.

Tax Outlook

The tax outlook remains uncertain after the Biden Administration failed during the spring to convince its entire Democratic Senate caucus to support its corporate tax plan. Senators Manchin (D-WV) and Sinema (D-AZ) were the key holdouts, by opposing major tax increases via the budget reconciliation process which requires a simple majority vote in the Senate. Note, too, that many House Democrats from high-tax states criticized the White House’s plan to not increase the $10,000 cap on state and local income tax deductions.

But the Biden team isn’t done. Thanks to negotiations led by Treasury Secretary Yellen, there appears to be an agreement being reached between most G20/OECD countries on a global tax deal. The OECD/G20 Inclusive Framework has two key elements. “Pillar One” appears mainly aimed at preventing major, multinational technology companies from avoiding taxes, by looking to tax profits based on the location of customers. “Pillar Two” would establish a minimum global corporate tax rate of 15%.

There are still some holdouts, and some of those countries’ ascent will be crucial to reach an agreement; and many technical details remain. But the White House is hoping that progress here will help persuade legislators in Washington that raising corporate tax rates in the US will not put American companies at a major competitive disadvantage… The threat of a higher US corporate tax rate remains; its probability appears to be 65% at the moment. We expect Senate Majority Leader Schumer to make a strong push in the coming weeks to pass a tax bill before the August recess.

U.S. Political Outlook

Three months ago, the Predicit betting market was giving Vice President Harris a 40% probability of becoming the 2024 Democratic Presidential Nominee, and President Biden 37%. But Harris’s political future took a significant blow in June, falling from 38% on June 1 to 30% as of July 9. The turn for the worse appeared to correlate with her trip to Central America on June 6.

Last week, Axios reported on significant concerns about Harris from inside the White House. According to Hans Nichols: “Some Democrats close to the White House are increasingly concerned about Harris’s handling of high-profile issues and political tone deafness, and question her ability to maintain the coalition that Biden rode to the White House.”

President Biden has mostly captured the points that Harris has lost in the betting market. But will Biden really run for re-election at the age of 81?

If Biden and Harris aren’t the nominees in 2024, there doesn’t seem to be an obvious alternative today. Every other Democrat is polling at 6% or less on Predictit. Will it be another Establishment Democrat or someone more aligned with the Progressive wing -- led by Senator Bernie Sanders and firebrand Congresswoman Alexandria Ocasio-Cortez, who leads the small group of House members called “The Squad”.

Harris’s performance in June elevates the importance of the special election on August 3 for an open congressional seat in Ohio. Progressives are backing Nina Turner, a former state senator and co-chair of Sanders’s 2020 presidential campaign; while the establishment is supporting Shontel Brown, chair of the Cuyahoga County Democratic Party… At the moment, Predictit is giving Turner a better than 80% probability of winning. If Turner wins, it forces the question: what will that do to the longer-term Democratic policy agenda? A more concerted effort toward higher taxes and Medicare for All?

DIAL IN FOR OUR MONTHLY

EVENT-DRIVEN CALL

Every 3rd Wednesday at 2:00pm EST

REGISTER FOR CALL

Paul Hoffmeister is chief economist and portfolio manager at Camelot Portfolios, managing partner of Camelot Event-Driven Advisors, and co-portfolio manager of the Camelot Event-Driven Fund (tickers: EVDIX, EVDAX).

B242 // Camelot Event-Driven Advisors LLC | 1700 Woodlands Drive | Maumee, OH 43537

Disclosures:

• Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), will be profitable or equal to past performance levels.

• This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. Camelot Event Driven Advisors can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

• Any charts, graphs, or visual aids presented herein are intended to demonstrate concepts more fully discussed in the text of this brochure, and which cannot be fully explained without the assistance of a professional from Camelot Portfolios LLC. Readers should not in any way interpret these visual aids as a device with which to ascertain investment decisions or an investment approach. Only your professional adviser should interpret this information.

• Some information in this presentation is gleaned from third party sources, and while believed to be reliable, is not independently verified.

• Camelot Event-Driven Advisors, LLC, is registered as an investment adviser with the United States Securities and Exchange Commission. Registration as an investment adviser does not imply any certain degree of skill or training. Camelot Event-Driven Advisors, LLC’s disclosure document, ADV Firm Brochure is available at http://adviserinfo.sec.gov/firm/summary/291798

Copyright © 2021 Camelot Event-Driven Advisors, All rights reserved.