by Paul Hoffmeister, Chief Economist

The spread of Covid around the world meaningfully decelerated during the last month.

Small caps and energy have recently outperformed large caps and tech.

No tax increases for now.

While tensions in Taiwan are the worst in more than 40 years, Biden Administration appears open to exemptions from the China trade tariffs that President Trump instituted.

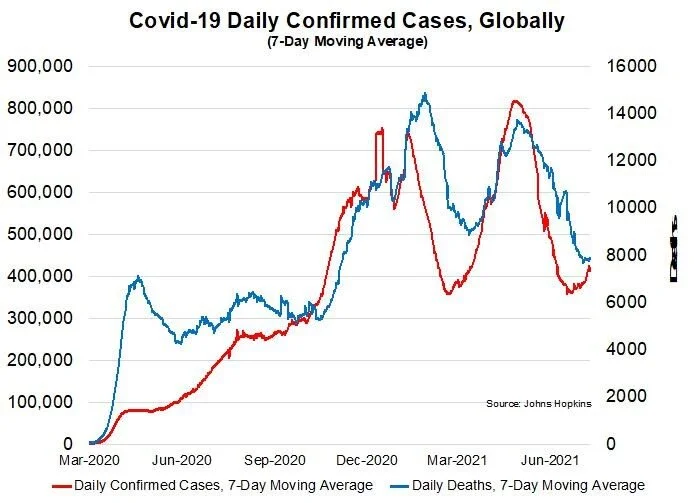

In terms of the economic data, the Covid recovery scenario remains in full force. The unemployment rate fell to 4.8%; the ISM manufacturing and services indices registered greater than 60, meaning that growth remains unusually robust historically speaking; and jobless claims have improved from September’s jump and close to their Covid lows. But, in our view, the most important data point of the last month was the significant decline in Covid cases and death rates.

As of the last week, the week-over-week rate of new Covid cases and deaths around the world was approximately 2.3 million and 37 thousand. This compares to nearly 4.1 million and 63 thousand at the end of August. In other words, according to the official global data, the spread of Covid meaningfully decelerated during the last month.

We note that some observers draw analogies with the 1917 pandemic and other historical pandemics, which had 3-4 waves before abating. While we cannot opine on the relevance of such analogies to the current pandemic, we note that the third wave seems to be behind us. Should the dynamic of such past pandemics be applicable to Covid, then this would indicate that the worst is behind us.

This positive news has correlated with some of the most sensitive financial indicators moving higher: the oil price and the 10-year Treasury yield. Between August 31 and October 11, the price of a barrel of oil (West Texas Intermediate) jumped from around $68.50 to over $80; while the 10-year yield jumped from 1.31% to 1.61%. This reflex suggests that financial markets are adjusting to the prospect of greater-than-expected economic activity and demand, which would also translate into Federal Reserve policymakers raising interest rates sooner-than-expected.

As mentioned last month, we expected small caps and the energy sector to outperform large caps and technology in the event that Covid data were to significantly improve. Between August 31 and October 8, the Russell 2000 and XLE exchange-traded fund returned -1.8% and +16.8%, respectively; whereas the S&P 500 and QQQ exchange-traded fund returned -2.9% and -4.9%, respectively. While a lot of discounting may have already occurred recently, this market behavior suggests that a further return to post-Covid normalcy should continue to favor these segments of the market.

This positive momentum does bring with it economic risk, notably in the form of inflation. While monetary inflation does not appear to be a problem today, with gold prices steadily drifting lower, and money supply and money velocity relatively tame, the supply chain dislocations of the last year and a half have created distortions, causing higher prices and higher inflation statistics. Early this year, we highlighted bottlenecks at the lumbermills and the resultant jump in lumber prices. At the moment, significantly more oil supply from within the United States does not appear to be forthcoming, and OPEC appears resistant to adding more supply than previously planned. As a result, the recent jump in oil prices (and energy prices generally) pose a significant risk to keeping statistical inflation data elevated, which in turn will likely pressure Fed policymakers to raise interest rates. This could ultimately spook financial markets, as we experienced in 2018.

Fiscal Policy:

Democratic centrists and progressives have so far failed to come to an agreement on a $500+ billion infrastructure bill and $3+ trillion tax and spending legislation.

The two most important holdouts have been Senators Joe Manchin and Kyrsten Sinema. While Sinema has been quiet publicly about where exactly she disagrees with her caucus, Manchin has been vocal about his concerns over such a large spending package being passed through the simple-majority, budget reconciliation process. At the same time, some swing district House Democrats are concerned about the tax increases being proposed.

Manchin recently revealed that he’d only support up to $1.5 trillion in new taxes. This would implicitly entail less tax increases, which could also win the support of other centrists in Congress. As a result, the White House and the Democratic leadership have pared back their tax and spend ambitions. For now, it doesn’t appear that a deal will be reached until year-end, if at all.

US-China Relations:

In her first major public speech, the new US Trade Representative Katherine Tai described the US-China relationship as “complex and competitive”. The last month was filled with evidence of that – militarily and economically.

At the beginning of October, the Chinese military broke records three times for the number of planes entering Taiwan’s Air Defense Identification Zone in a day, and Taiwan’s defense minister described his country’s tensions with China to be at their worst point in over four decades. Then, last weekend, Xi Jinping said "achieving unification through peaceful means is most in line with the overall interests of Chinese people, including Taiwan compatriots…those who forget their heritage, betray their country, and seek to break up their country, will come to no good end." At the same time, Taiwan publicly acknowledged the presence of US troops conducting military exercises in-country.

While the issue of Taiwan looks to be increasingly dangerous, Ambassador Tai may have conveyed conciliatory signals by announcing that the Biden Administration was considering a targeted tariff exclusion process for US importers of Chinese goods on 549 import product categories. The US Trade Rep’s office will accept public comments in the coming weeks. While Trump Administration duties remain in place today, it appears that those duties could be alleviated soon – for some companies.

Current Market-based Political Outlook:

According to Predictit betting markets, the current probability of Republicans regaining control of the House and Senate in the 2022 midterms are 73% and 55%, respectively. President Trump’s probability of being the 2024 Republican nominee has notably sky-rocketed to 48%, from 30% in July… As for who will win the 2024 presidential election: Trump is at 30%, President Biden 28%, Vice President Harris 15%, and Governor Desantis 13%.

Summary:

In summary, the US economy is performing well, Covid data has substantially improved in recent months, and the tax threat to financial markets has abated. This positive news has correlated with strength in some of the most risk-sensitive segments of the financial market. US-China remains an important complicated, long-term variable to monitor: both militarily and economically. While Taiwan is becoming a major proxy of US-China strategic interests in the region, the Biden Administration may rescind some of the Trump trade tariffs in the coming months.

DIAL IN FOR OUR MONTHLY

EVENT-DRIVEN CALL

Every 3rd Wednesday at 2:00pm EST

REGISTER FOR CALL

Paul Hoffmeister is chief economist and portfolio manager at Camelot Portfolios, managing partner of Camelot Event-Driven Advisors, and co-portfolio manager of the Camelot Event-Driven Fund (tickers: EVDIX, EVDAX).

Camelot Event-Driven Advisors LLC | 1700 Woodlands Drive | Maumee, OH 43537 // B267

Disclosures:

• Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), will be profitable or equal to past performance levels.

• This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. Camelot Event Driven Advisors can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

• Any charts, graphs, or visual aids presented herein are intended to demonstrate concepts more fully discussed in the text of this brochure, and which cannot be fully explained without the assistance of a professional from Camelot Portfolios LLC. Readers should not in any way interpret these visual aids as a device with which to ascertain investment decisions or an investment approach. Only your professional adviser should interpret this information.

• Some information in this presentation is gleaned from third party sources, and while believed to be reliable, is not independently verified.

• Camelot Event-Driven Advisors, LLC, is registered as an investment adviser with the United States Securities and Exchange Commission. Registration as an investment adviser does not imply any certain degree of skill or training. Camelot Event-Driven Advisors, LLC’s disclosure document, ADV Firm Brochure is available at http://adviserinfo.sec.gov/firm/summary/291798

Copyright © 2021 Camelot Event-Driven Advisors, All rights reserved.