by Paul Hoffmeister, Portfolios Manager and Chief Economist

Last month, we explained that interest rates were expected to stay higher for longer because inflation had become stubborn. Core PCE was holding near 2.8% in recent months, after declining nicely from 5.5% since 2022. As a result, the market had come to expect only one or two quarter point rate cuts by year-end, compared to as many as four or five at the beginning of this year.

We also added that the Fed’s reaction function for deciding whether and to what degree to cut rates later this year will likely be predicated on the core PCE falling convincingly toward 2% and/or the unemployment rate jumping meaningfully higher than 4%.

Last Friday, the unemployment rate increased to 4%; a level not seen since Q1 2022. From an economic and market perspective, the level may not be as important as the rate of change. A year ago during Q2 2023, the unemployment rate hovered around 3.6%. The reason that’s important is because, based on the Sahm Rule, it’s likely that the US economy will be entering recession if the rate soon reaches 4.1-4.2%. (According to the St. Louis Federal Reserve, the Sahm Rule “signals the start of a recession when the three-month moving average of the national unemployment rate rises by 0.50 percentage points or more relative to the minimum of the three-month averages from the previous 12 months.")

While there has recently been some contradictory labor market data indicating that employment is actually increasing, we believe that the rising unemployment rate is closer to the truth and that the labor market and economy are weakening at the margins. In our view, this would be much more consistent with a slew of macroeconomic indicators and signals showing deterioration; such as the inverted yield curve, relatively weak leading economic indicators, cautious lending surveys, weak regional Fed data, and qualitative feedback published in the Fed Beige Book from economic participants across the country.

U.S. Unemployment Rate (recessions highlighted in red). Source: Bloomberg.

The chart above illustrates the unemployment rate since 1988 and periods of recession (highlighted in red columns). Indeed, upturns in the rate like we’re seeing today, strongly suggest an economic contraction on the horizon.

Notwithstanding, why does the question of recession matter to investors? After all, some US stock market indices (and other foreign indices) have recently hit all-time highs, certain credit spreads are relatively tight, and credit market conditions are seemingly excellent.

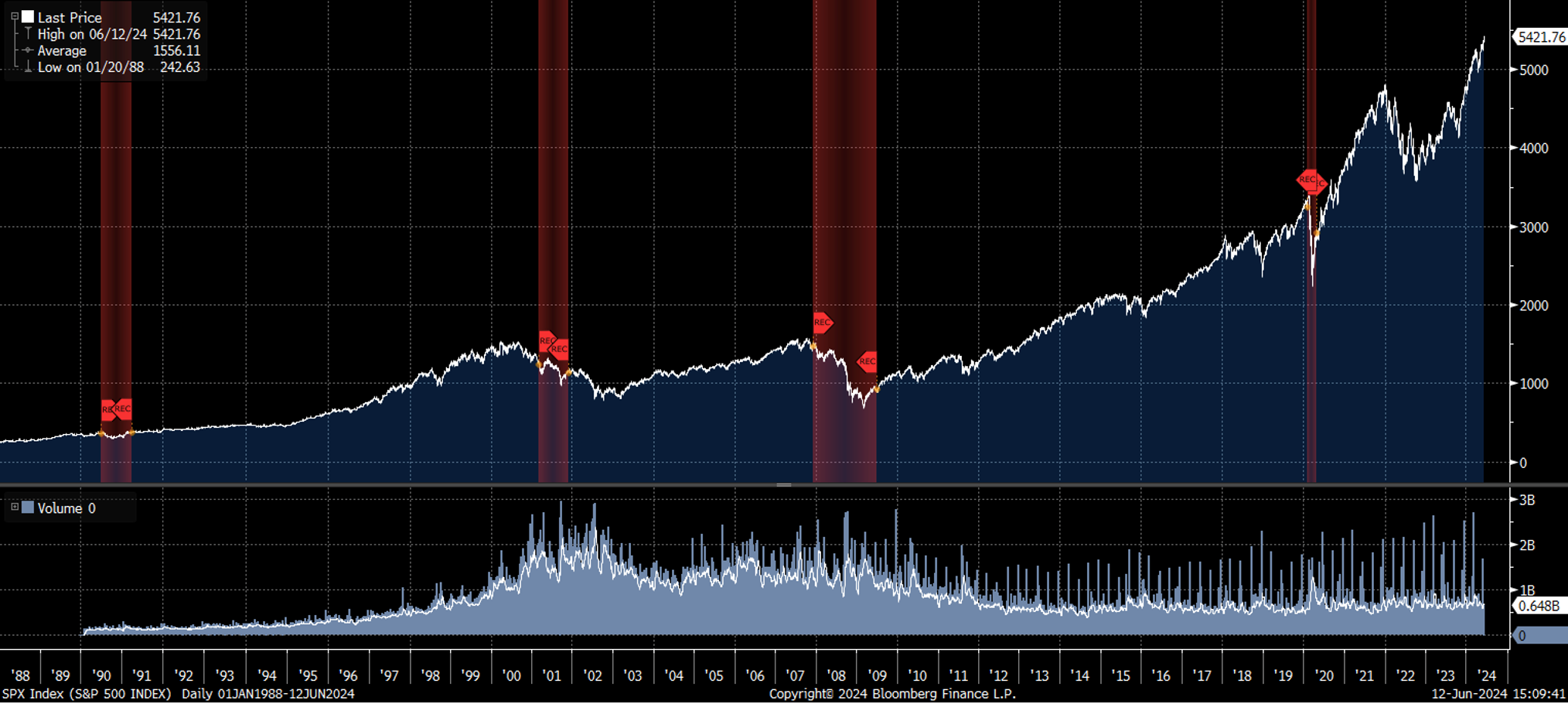

It’s relevant because economic contraction tends to correlate with not only slower earnings growth but also significant downside risk in equity indices. For example, within the context of the 2001 recession, quarterly earnings in the S&P 500 fell from $14.68 in Q3 2000 to $10.43 in Q1 2002. (Bloomberg) Within the context of the 2007-2009 recession, quarterly earnings fell from $24.55 in Q3 2007 to as low as $5.87 in Q1 2009. (Bloomberg) Based on the historical evidence, economic contractions can meaningfully impact the S&P 500.

Naturally, if earnings decline, stock valuations and stock prices are threatened. Between Q3 2000 and Q1 2002, the S&P 500 lost nearly 28%. Between Q3 2007 and Q1 2009, it lost almost 56%.

S&P 500 Index (recessions highlighted in red). Source: Bloomberg.

A lot of attention is being paid on Fed policy, inflation and employment data. Of course, a 2024-2025 recession isn’t pre-determined. But the history of the last few decades suggests that a slowly deteriorating labor market, which is what we might be seeing now, raises the specter of recession and weaker equity markets.

Click Below to Register for:

CEDA’s Monthly Event-Driven Call!

2nd Tuesday each month. 2pm with 2PMs. 22 Minutes.

Paul Hoffmeister is Chief Economist and Portfolio Manager at Camelot Portfolios, managing partner of Camelot Event-Driven Advisors (CEDA), and co-portfolio manager of the Camelot Event-Driven Fund (EVDIX • EVDAX).

Camelot Event-Driven Advisors LLC | 1700 Woodlands Drive | Maumee, OH 43537 // B573

Disclosures:

• Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), will be profitable or equal to past performance levels.

• This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. Camelot Event Driven Advisors can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

• Any charts, graphs, or visual aids presented herein are intended to demonstrate concepts more fully discussed in the text of this brochure, and which cannot be fully explained without the assistance of a professional from Camelot Portfolios LLC. Readers should not in any way interpret these visual aids as a device with which to ascertain investment decisions or an investment approach. Only your professional adviser should interpret this information.

• Some information in this presentation is gleaned from third party sources, and while believed to be reliable, is not independently verified.

• Camelot Event-Driven Advisors, LLC, is registered as an investment adviser with the United States Securities and Exchange Commission. Registration as an investment adviser does not imply any certain degree of skill or training. Camelot Event-Driven Advisors, LLC’s disclosure document, ADV Firm Brochure is available at http://adviserinfo.sec.gov/firm/summary/291798

Copyright © 2024 Camelot Event-Driven Advisors, All rights reserved.