by Thomas Kirchner & Paul Hoffmeister

August 15 marked Napoleon’s 250th birthday. Doomsayers used that anniversary to compare the failure of his pan-European empire to the current state of the EU. But we believe that the comparisons with and predictions of the demise of the European Union completely miss the point of where today’s EU stands. Without question, the EU has its problems, including a stifling bureaucracy and policies that suffocate growth and innovation. However, missed in most criticisms of the EU and predictions about its future is the consideration of its significant net benefits that will make it survive longer than many critics currently believe.

European empires

The present-day EU differs from prior pan-European empires, whether Napoleonic or that of Charlemagne a millennium earlier, in its voluntary nature. It is not an empire assembled through war. Napoleon’s empire building is estimated to have cost six million lives, and massacres and ethnic cleansing ordered by Charlemagne are likely to have had a lower death toll only because of a lower overall population at the time.

The EU did not conquer its member states. Instead, states couldn’t wait to join. For Eastern Europe’s former Soviet vassals, EU membership was a major step into modernity, not a defeat in the face of an overwhelming enemy. Comparisons between the EU and failed empires are not just silly, they are plain wrong.

Aristocrats, scholars and monks

A better analogy for the EU today than short-lived empires are the lives of Europe’s aristocracy up to the French revolution. They constituted a European Union of aristocrats of sorts, with a common market for crowns and titles. While it is tempting to compare fallen empires to today’s because we tend to think in national categories with each country having more or less well-defined borders, that was only a secondary part of how people thought long ago. While the majority of the population lived in servitude and was unable to leave the land, several superstructures transcended borders of towns and principalities.

For royalty and aristocrats, what we would refer to as national origin today played no role in the award of a title. It was not uncommon to see a crown or other title conveyed upon someone with no attachment to the land. Leopold I became the first King of Belgium upon its independence, after he turned down the crown to the throne of Greece and after having served in the Russian army. [i] Coming from the German dynasty of Saxe-Coburg-Saalfeld, he had no relation to either of these countries. Similarly detached from his territory was Frederic II of Prussia, who is said to have spoken only broken German, which didn’t matter because the official Court language was French anyway, and he was fluent in that. [ii]

The clergy and laic scholars led lives similarly detached from what we would call national origin today. Monastic orders established their own rules and regulations that formed communities across the continent. Scholars and students in universities were afforded a special status by the church equivalent to clergy and were encouraged to spread knowledge across Europe, in particular by the exemption from the residency requirements applicable to clergy. In fact, the EU refers to this medieval scholarly mobility to justify one of its fundamental principles, freedom of movement. The business community has a similarly Europe-wide history to look at, with Venetian bankers and traders or their Dutch counterparts dominating the continent’s trade routes during different time periods.

These pan-European structures existed long before the creation of the nation state. Therefore, the idea that the nation state is a more appropriate framework for political, economic and intellectual life than the EU is not supported by history. In fact, most of these pan-European behaviors disappeared only once the French revolution eradicated medieval societal structures; and in its wake the nation state took hold as the new normal.

The nation state was an artificial creation, so artificial that the French had to spend much of the 19th century teaching their population the official French language. People spoke Basque, Breton, Flemish, Occitan or numerous other languages before the forced adoption of French as the national language. It is important to remember that medieval pan-European structures were destroyed only by the establishment of these artificial nation states. The often-repeated criticism today that a globalized elite had taken control of society and was trying to eradicate the nation state implies that it would have been normal in the past that such elites felt constrained by nation states, when in reality no such limitations existed.

The fact is, leaders thinking beyond national borders today is a return to historical normalcy in Europe after two centuries of nation state exceptionalism. Hence, today’s EU is by no means an artifact but a return to wide networks that grew naturally when they weren’t inhibited by artificial borders.

Tangible benefits of EU membership

In the present day, EU membership conveys to countries clear and tangible benefits, which is the main attraction for joining, as well as a major hurdle for leaving.

There is not just the obvious benefit of direct access to a market of over 500 million consumers, which is almost twice the size of the U.S. market. EU membership also comes with a set of unified rules and regulations that can be implemented in domestic regulations without constituting an impediment for market access. For smaller countries, this is a particularly significant benefit.

Imagine if companies had to adhere to 26 different national regulations to access 500 million consumers. Most likely, companies would create versions of their products and services only for the top markets and simply ignore smaller countries such as Slovenia (pop. 2 million), Bulgaria (pop. 7 million), Malta (pop. 460,000) or Finland (pop. 5 million).

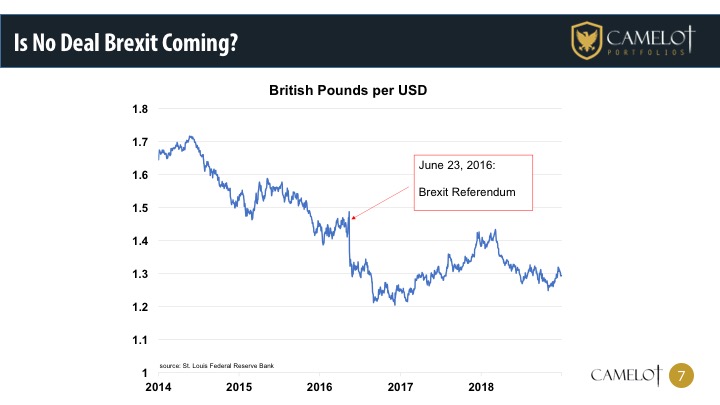

Almost two thirds of EU member States have a population of 10 million or less. [iii] These countries would not be able to function in the same manner as large, developed countries if it were not for EU membership. Any advantages from a higher degree of sovereignty from leaving the EU would soon be offset by their mutation into banana republics. Brexit is a viable option for a large member state like the UK and potentially Italy, but it could be economic suicide for smaller member countries -- and even the threat of leaving lacks credibility.

Contrary to the view of some critics, EU membership restores some degree of sovereignty to smaller member countries that would otherwise be lost. Consider approval of new drugs, for example. As an EU member, a small country has some say in how drugs get approved in the EU. However, as non-EU members, a country like Portugal (pop. 10 million) [iii] would probably be last in line for large pharmaceutical companies to introduce new drugs. So its citizens would either not get the benefit of these drugs for years after their introduction in larger countries. Alternatively, these smaller countries could rubber stamp the approval in a larger neighbor, which of course means that they will have no say at all in the process. EU membership conveys clear advantages over going solo. The departure of these smaller, poorer countries from the EU is less feasible than a secession of Manhattan from the U.S.

Common market in lieu of a free trade zone

The EU and its predecessors starting with the 1951 European Coal and Steal Community (ECSC) between Belgium, France, Italy, Luxembourg, the Netherlands, and West Germany [iv] were deliberately designed as common markets rather than free trade zones. In the eyes of its founders, free trade zones gave their members too much leeway in favoring domestic firms over importers by blocking market access through consumer protection and safety, environmental or myriad other regulations. A good example of such non-tariff barriers is Japan’s treatment of imported Perrier water bottles, which for years were required to feature health warnings, while domestically-bottled water that did not go through customs did not have such warnings. Not surprisingly, Perrier struggled to compete with Japanese bottled water despite reaping the benefits of a free trade agreement.

Crucially, the ECSC was under the control of a High Authority, the predecessor to today’s European Commission, as a supranational executive that was to enforce the treaty. Unlike in a free trade area, where enforcement and implementation are both national responsibilities that open the door to abusive and manipulative practices, the supranational character of the enforcement body, supplemented by a judiciary and parliamentary oversight body, eliminated room for gaming the system and simultaneously kept the system current. The latter point is particularly important for the stability of common markets compared to free trade zones. This institutional framework, which has been modernized in today’s EU from the 1951 ECSC, is what makes the common market function and helps to overcome attempts of individual nations to gain an advantage.

The recent NAFTA renegotiation illustrates this distinction well: NAFTA remained static since it was signed by President Clinton in 1993. It took punitive tariffs and the threat of even more punitive tariffs to get the parties to agree to update the treaty to reflect the changes in the economy that had occurred over the quarter century since its inception. Now imagine if the EU lacked its institutional framework and instead had to renegotiate its free trade pact bilaterally in a similar way as the U.S. did with Canada and Mexico. What worked between three nations in the Americas only after major trade frictions would be completely impractical in a 28-nation European free trade block. It is the EU’s institutional framework that keeps the common market updated, relevant and practical.

From a common market to a common bureaucracy

That is not to say that the EU is not deeply troubled. The European Commission follows the universal bureaucratic logic of regulatory creep. Thus, the common market has morphed into a common bureaucracy.

This logic ends up producing ridiculous rules from time to time, such as the attempted regulation of the curvature of cucumbers, bananas and other produce which was scrapped after a public uproar in 2008; or the classification of carrots as a fruit because otherwise the interaction with another rule would have prevented the Portuguese from making carrot marmalade, a local delicacy.

Part of the problem is the dominance of the bureaucracy over the institutions. Parliament would normally be the institution to limit bureaucratic excesses. But the European Parliament is caught in a chicken-and-egg dilemma: because it has little power, often “misfits” volunteer to be elected as Members of the European Parliament (MEP). And because of the preponderance of misfits among MEPs, not many want to give the parliament more power. Many MEPs represent fringe opinions in their political parties, and fringe parties use the European Parliament as a platform to publicize their agendas. In the last election, a record number of MEPs with colorful biographies were elected, including two from Germany’s joke party Die Partei whose leader refers to himself as a “demotivation coach” and stated openly he was running for office only to collect the generous perks. Therefore, the reluctance to cede more powers to this institution is understandable, and as a result its ability to reign in the executive remains limited.

Similarly, national parliaments are too far removed from the decision-making process. The European Commission proposes a new regulation to a council composed of government ministers, who then approve, reject or modify the regulation. When something proves to be unpopular, ministers will blame “Brussels” for it, even though they signed off on it themselves. National parliaments, for a variety of mostly practical bureaucratic reasons, fail to oversee their ministers’ and bureaucrats’ actions in the council. As a result, the national executives like to use the EU to implement policies that would have little chance of going through national parliaments.

Unfortunately, it is unlikely that these shortcomings will be resolved anytime soon. What would be needed is a complete deregulation of the common market coupled with a different approach. Rather than mandating how member states should write their rules, the European Commission should designate what cannot be regulated. This would dramatically decrease bureaucratic and compliance complexity. However, short of a trailblazing, pro-growth political leader taking over the EU Presidency, common sense deregulation remains elusive.

Follow the money

Don’t be fooled by headlines about the potential dangers to EU cohesiveness due to discord over immigration or other hot topic policies between conservative Eastern European governments and center-left Western European ones.

Consider Poland and Hungary, whose governments are the more vocal opponents of many EU policies. They receive 2.67% and 3.43% of their gross national income as transfers from the EU while spending less than 0.70% of their gross national income on EU membership. They are net beneficiaries of EU transfers to the tune of 2-2.5%, a non-negligible amount of subsidy that they receive annually. Despite their belligerent rhetoric over the political topic du jour, it would be financially ruinous for these net recipients to leave the EU. Compare that to the UK, which paid 0.46% into the EU while receiving only 0.28%, and where Brexit leads to a small net positive fiscal position [v].

Therefore, even the most vocal opponents of EU policy have little incentive for leaving the EU or seeing its disintegration by further departures. While direct subsidies are a substantial financial benefit to poorer and smaller member states, the main economic benefit comes in the form of the common market, without which many of the countries would be condemned to remaining economic backwaters. Therefore, warnings of a potential EU disintegration are pure hypotheticals that investors should take with a high degree of skepticism.

Thomas Kirchner has been responsible for the day-to-day management of the Camelot Event Driven Fund since its 2003 inception. Prior to joining Camelot he was previously was the founder of Pennsylvania Avenue Advisers LLC and the portfolio manager of the Pennsylvania Avenue Event-Driven Fund. He is the author of 'Merger Arbitrage; How To Profit From Global Event Driven Arbitrage.' (Wiley Finance, 2nd ed 2016)

Paul Hoffmeister is chief economist and portfolio manager at Camelot Portfolios, managing partner of Camelot Event-Driven Advisors, and co-portfolio manager of Camelot Event-Driven Fund (tickers: EVDIX, EVDAX).

[i] “Leopold I, King of Belgium.” Encyclopedia Britannica, Updated December 12, 2018.

[ii] “Frederic II, King of Prussia.” Encyclopedia Britannica, Updated August 13, 2019.

[iii] Eurostat. Table Code: tps00001.

[iv] Etienne Deschamps, “The beginnings of the ECSC.” CVCE.eu European Navigator, 2019.

[v] “EU member countries in brief” on Europe.eu.

Disclosures:

• Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), will be profitable or equal to past performance levels.

• This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. Camelot Event Driven Advisors can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

• Originally published on http://www.camelotportfolios.com/commentaries